Testing a car loan in advance isn’t just smart, it’s essential.

Skipping the simulation step often leads to deals that feel manageable on paper but collapse under real-world pressure. By using an online loan calculator, you preview repayment totals, interest charges, and monthly obligations with clarity.

![5 Genuine Online Data Entry Jobs Without Investment [2025 Updated]](https://expable.com/wp-content/uploads/2023/01/Online-Data-Entry-Jobs-Without-Investment-300x183.jpg)

This gives you the power to reject mismatched terms, choose the best lender, and stay within a budget that protects your cash flow from the start.

Online Simulation Protects Your Budget

Rushing into a car loan without testing numbers first often leads to payments that outrun monthly cash flow, which means stress, missed due dates, and damaged credit.

Running accurate simulations online provides an unbiased preview of interest costs, repayment timelines, and the total price you will shoulder, allowing you to negotiate from a position of strength and select terms that fit comfortably within regular income.

Fundamentals of Car-Loan Simulation

Before entering figures in any calculator, gather the five variables every simulator demands:

| Variable | What to Collect | Where to Find It |

| Vehicle price | Retail list price + destination charges + common add-ons | Official brand site, dealer quote |

| Down payment | Planned cash portion (often 20 %–50 %) | Personal savings plan |

| Loan term | Desired repayment length in months (12–72) | Budget forecast |

| Annual percentage rate (APR) | Best rate quoted by banks, credit unions, or manufacturer promos | Pre-approval offers, lender websites |

| Fees & insurance | Documentation, processing, registration, and annual premium estimates | Dealer disclosure sheet, insurer quote |

Having accurate inputs ensures the simulator mirrors real-world costs rather than optimistic guesses.

Selecting a Reliable Online Calculator

Many websites promise quick quotes; only a few deliver detailed amortization and flexible scenarios. Evaluate each tool using four criteria:

- Multi-term slider: Adjust months and watch payments update live.

- Fee fields: Include processing fees, insurance, or taxes instead of hiding them.

- Amortization table export: Download a PDF or spreadsheet for later comparison.

- Currency and rate editing: Change APR and switch between local currencies when needed worldwide.

Top options:

- Bank-hosted calculators: Local banks publish branded calculators with exact rates; useful for region-specific accuracy.

- Marketplace simulators: Platforms such as AutoDeal, Edmunds, or Carbuyer aggregate multiple banks and display side-by-side offers.

- Spreadsheet templates: Excel or Google Sheets templates allow complete manual control, ideal when multiple fees or balloon payments apply.

Step-by-Step Simulation Workflow

A structured routine eliminates data entry errors and exposes hidden costs early, therefore, follow each step without skipping.

- Open two calculators in separate tabs: cross-checking prevents reliance on a single engine.

- Insert identical core data: price, down payment, term, and APR.

- Add administration fees and prepaid insurance where fields exist; if absent, shift to a tool that allows custom costs.

- Generate and download the amortization schedule: note principal vs interest split.

- Alter one variable at a time: extend term by six months, raise down payment by five percent, or insert a higher APR, then record the new monthly figure.

- Plot the highest monthly installment against net income – payment plus insurance plus fuel should not exceed fifteen percent of take-home pay.

- Repeat the process with at least one alternative vehicle – a lower trim or used model may fit better without sacrificing core needs.

- Save PDFs or screenshots in a dedicated folder ready for negotiation at the dealership or bank.

Interpreting Simulator Results

A spreadsheet or PDF will highlight three headline numbers:

| Metric | Meaning | Action if Uncomfortable |

| Monthly payment | Cash leaving your account each period | Raise down payment or lengthen term slightly |

| Total interest | Price paid for borrowing money | Shop for lower APR or shorten term |

| Total repayment | Vehicle cost plus all finance charges | Compare with cash purchase savings |

Focus on the monthly figure first. If it already strains your budget before adding fuel, maintenance, and insurance, restructure the loan or pick a different model. Next, evaluate total interest.

High interest erodes resale gains, especially on rapid-depreciation vehicles, so tightening term length often saves thousands. Finally, examine total repayment to decide whether financing still beats waiting and saving for a cash purchase.

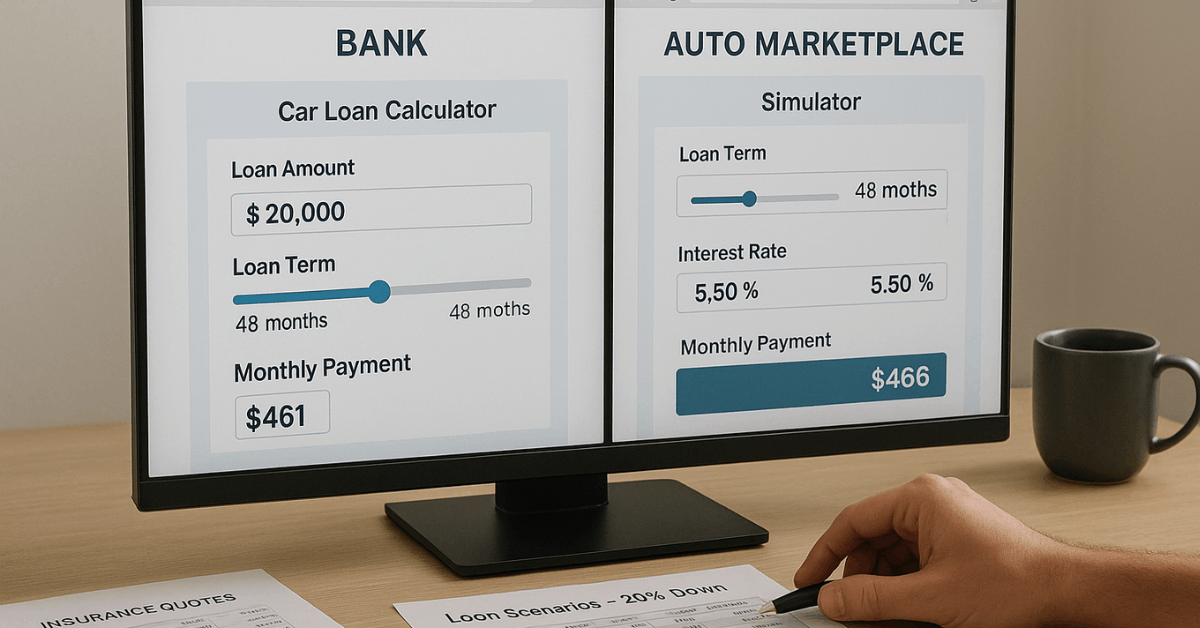

Bank vs Dealer Simulation: Key Differences

Before approving any loan, run distinct simulations for each channel.

| Factor | Direct Bank Financing | Dealer-Arranged Financing |

| Typical APR | Usually lower, no markup | May include dealer spread |

| Down-payment requirement | 20 % minimum standard | Promotional low or zero down possible |

| Processing speed | Slower if paperwork incomplete | One-stop same-day approval |

| Negotiation leverage | Strong; you arrive pre-approved | Weaker; dealer controls lender selection |

| Extra incentives | Possible bank loyalty discounts | 0 % APR or free add-ons on select models |

Simulation Strategy

Simulate the bank offer first, then negotiate at the dealership armed with those numbers. If the dealer can beat or match the net cost (including hidden fees) through captive financing, consider the convenience.

Document to Prepare for a Smooth Approval

Skimming requirements leads to rejection or delays. Prepare copies, physical and digital, of the following before submitting any application worldwide:

- Two government-issued IDs with signature and photo.

- Proof of residence (utility bill dated within three months).

- Employment or business income documents:

- Salaried: three latest pay slips and tax certificate.

- Self-employed: audited financials, business registration, and recent bank statements.

- Dealer quotation indicating vehicle price, variant, and chassis number.

- Home ownership or rental agreement for stability evidence.

- Same complete set for any co-maker or guarantor.

Upload scanned copies to the online portal and label files clearly to speed underwriting.

Common Simulation Mistakes and How to Avoid Them

Address each pitfall during simulation to avoid costly surprises later.

| Mistake | Consequence | Corrective Action |

| Ignoring fees beyond principal and interest | Understates monthly burden | Input every charge into a comprehensive spreadsheet |

| Using promotional 0 % APR for entire term without checking qualifiers | Surprise high rate if requirements unmet | Verify tenure limits, balloon clauses, and model restrictions |

| Overestimating resale value in balloon scenarios | Balloon shortfall at maturity | Use conservative depreciation tables from third-party valuation guides |

| Failing to test worst-case interest rise on variable-rate offers | Payment shock in year two or three | Simulate three percent higher APR to gauge affordability |

| Forgetting insurance premium escalations | Budget squeeze after first year | Add projected annual increases into five-year cost map |

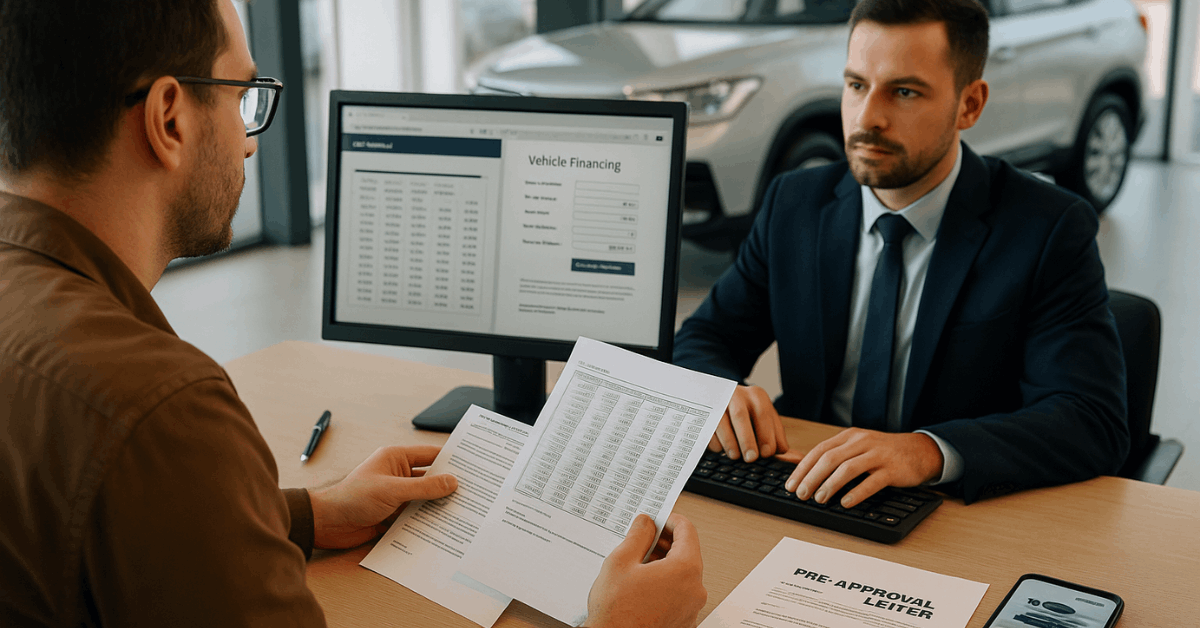

Negotiation Leverage Generated by Simulation Data

Arriving at the showroom with printed amortization tables and pre-approval letters transforms you from passive shopper to informed buyer. Use data for:

- Payment cap: decline offers exceeding the validated comfortable monthly figure.

- Interest-rate challenge: show the bank quote and request dealer rate matching.

- Extended-warranty evaluation: calculate added months and confirm payment rise fits budget.

- Add-on filtering: demonstrate total repayment difference with and without optional accessories, then accept only essential items.

When sales staff recognize you understand financing math, they typically present clearer, more competitive packages.

Extra Tips to Boost Approval Odds

Maintain a stable employer or business income record for at least two years; sudden job changes can trigger rejection. Lower revolving credit utilization below thirty percent in the three months before application to raise credit score.

Avoid multiple hard inquiries by using marketplace pre-qualification with soft pulls first, then choose one or two full applications. Increase down payment by five percent if initial simulation shows tight affordability; the lower monthly obligation often turns an initial “no” into a “yes”.

Opt for auto-debit repayment; lenders reward automatic deduction with marginally lower APR in many regions.

Applying Simulation Insights to Used-Car Loans

Pre-owned vehicles attract higher fixed rates due to higher lender risk. Counter this by:

- Shortening the term to forty-eight months or less to reduce cumulative interest.

- Paying first monthly installment upfront to shave the APR with some lenders.

- Selecting units under five years old with full service records; newer cars qualify for better rates.

Run separate simulations for used and new versions of the same model to confirm which path delivers the most value over the ownership period.

Comprehensive Cost-of-Ownership Spreadsheet

Purchase price is one line item; comprehensive simulation includes every recurring cost over at least five years.

| Category | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Loan installments | Input from simulator | ||||

| Insurance premium | Quote + expected increase | ||||

| Fuel (average km × price per liter) | |||||

| Maintenance & service | Scheduled visits | ||||

| Registration & road tax | |||||

| Total annual outlay | Auto-sum |

Populate this table after you finish simulations to see full cash-flow demands, then choose the model and term creating the healthiest buffer in every year.

Conclusion

Car-loan calculators transform complex finance arrangements into transparent numbers you can test, tweak, and trust. Collect accurate data, run multiple scenarios, and scrutinize fees before meeting lenders or dealers.

When every variable has been simulated—monthly payment, total interest, down payment impact, and ownership costs—finalizing a loan becomes a strategic decision rather than a financial leap of faith.

Apply these disciplined steps, maintain a realistic budget cushion, and drive away confident the payment plan supports long-term financial stability instead of undermining it.