Buying a motorcycle without paying the full price upfront is entirely feasible once you master online financing simulators.

You gain clear visibility into monthly obligations, total interest, and optimal repayment terms, which means you avoid taking on debt that strains your budget later.

Use the guidance below to run accurate simulations, compare providers, and choose a loan structure that aligns with your income and riding plans.

Benefits of Simulating Motorcycle Financing Online

Hidden costs often derail well-meant purchase plans; therefore, running simulations before signing a contract protects your wallet and expands your negotiating power.

- Real-time cost preview lets you adjust down payments or terms until installments fit your income comfortably.

- Transparent comparison between fixed and variable rates shows which option costs less over time.

- Instant access worldwide removes the need to visit multiple branches, saving travel time and reducing pressure from sales staff.

- Bargaining leverage emerges once you know market-standard rates, allowing you to request better conditions at dealerships or banks.

- Budget alignment occurs because you can integrate insurance premiums and maintenance estimates into the same cash-flow model.

Essential Data You Need Before Running a Simulation

Successful calculations depend on reliable figures. Gather the following information in advance to prevent repeated entries and inconsistent outputs:

- Motorcycle price including delivery, registration, and optional accessories you cannot live without.

- Desired down payment as a percentage or exact amount; most lenders worldwide expect at least twenty percent.

- Loan term in months; typical ranges span twelve to sixty but can extend further in certain markets.

- Quoted annual interest rate (APR) from at least three providers so you can test multiple scenarios.

- Expected insurance cost because combining that fixed expense with the installment gives a more realistic monthly total.

- Administrative fees covering documentation, credit analysis, or early settlement penalties.

Keep these numbers in a spreadsheet or note-taking app. Accurate inputs drive accurate forecasts.

Online Simulation Tools Worth Testing

Global riders have two main categories to choose from: web-based calculators and mobile applications. The table below summarizes five popular options you can access at no cost.

| Tool | Platform | Key Strength | Geographic Availability | Offline Export |

| NAFIN Loan Calculator | Web | Detailed amortization table | Latin America focus, works worldwide | |

| Credit Simulator (Android) | App | Push reminders for due dates | Worldwide | CSV |

| IQ Loan Calculator (Android / iOS) | App | Multi-scenario quick switch | Worldwide | Charts |

| Bank-Provided Estimators | Web | Real-time rate update | Region-specific | None |

| Spreadsheet Templates (Excel / Sheets) | Desktop & Web | Full formula control | Worldwide | Full editing |

Each option uses the same basic variables, yet interface design, reporting depth, and export formats differ. Test at least two calculators to cross-check figures before relying on the results.

Step-by-Step Guide to Running Your First Simulation

Upfront organization streamlines the process and minimizes input errors.

- Open the calculator that offers your preferred language and currency.

- Enter the motorcycle price inclusive of taxes and delivery.

- Input your down payment and confirm that the field accepts either currency values or percentages.

- Select the repayment frequency—monthly, quarterly, or semi-annual—because lenders sometimes reward less frequent installments with marginally lower rates.

- Insert the annual interest rate exactly as quoted; avoid rounding to keep accuracy high.

- Choose your loan term by typing the total months or years.

- Add optional insurance or administrative fees if the calculator provides custom fields.

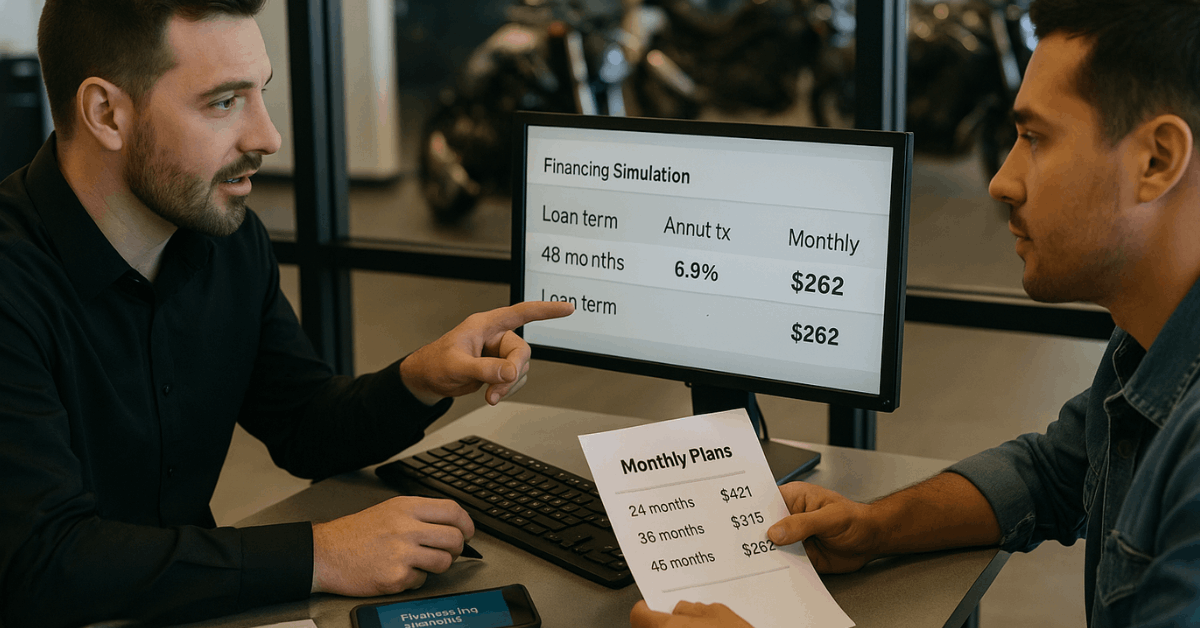

- Click calculate and review total repayable amount, per-period installment, and cumulative interest.

- Modify one variable at a time—for example, shorten the term by six months—then recalculate to observe the cost difference.

- Save or export the amortization schedule so you can reference exact due dates and interest components while negotiating.

Reading the Results and Making Smart Adjustments

Simulators often highlight three financial indicators: monthly installment, total interest, and total repayment. Your goal is to balance affordability with overall cost.

- Excessive monthly pressure? Increase the down payment or extend the term cautiously.

- High total interest? Shorten the term or consider a fixed rate if variable projections climb steeply.

- Insurance shock? Request multiple quotes or select models with lower theft or repair risk.

Iterate until the combined figure, installment plus insurance, equals no more than ten to fifteen percent of your disposable monthly income worldwide. This threshold keeps emergency savings intact.

Financing Variables That Shape Your Payment

Cash-flow control starts with understanding every lever that lenders adjust.

- Nominal vs Effective APR: Effective rates include compounding, fees, and taxes, making them more reliable for comparison.

- Fixed vs Variable Interest: Variable rates start low but may spike due to inflation or policy changes, inflating long-term costs.

- Loan Term Length: Longer terms flatten monthly installments yet inflate cumulative interest; shorter terms do the opposite.

- Residual Value (Balloon Option): Some contracts postpone a large final payment, lowering initial installments but requiring disciplined saving to cover the balloon.

- Early Repayment Penalties: Certain agreements charge a fee for settling ahead of schedule, reducing flexibility if your income rises.

Model each variable within the simulator to see how your repayment curve shifts.

Requirements You Should Expect

Financial institutions across continents enforce similar baseline criteria:

- Minimum age of eighteen (twenty-one in select jurisdictions).

- Verifiable income meeting the lender’s minimum ratio of installment to salary.

- Positive credit history or robust guarantor.

- Proof of address and national identification.

- Life or credit insurance covering outstanding balance in case of death.

- Down payment around twenty percent of the motorcycle’s invoice value.

Prepare digital scans of payslips, tax returns, and bank statements before applying online to accelerate approval.

Seven Practical Tips for First-Time Buyers

A successful purchase combines accurate simulation with disciplined fieldwork. The pointers below streamline your journey from screen to saddle.

- Secure pre-approval from a bank or credit union to enter showrooms with clear spending limits and stronger bargaining leverage.

- Set a strict ceiling using affordability calculators that include estimated insurance and maintenance, not just the loan installment.

- Research models comprehensively online—focus on engine size, ergonomics, and fuel consumption—then shortlist only units within budget.

- Request multiple insurance quotes early; the premium sometimes equals a quarter of the monthly loan, especially for high-performance bikes.

- Visit at least two dealerships to inspect chosen models physically, comparing out-the-door pricing that bundles taxes, registration, and mandatory accessories.

- Test-ride each contender to confirm fit, handling, and potential mechanical issues before any paperwork.

- Review the contract line by line, covering fees, warranty conditions, and accessory charges, before you sign and transfer the down payment.

Follow these steps sequentially to eliminate impulse decisions and maintain full cost transparency.

Mistakes That Derail Financing Plans

Avoid the following errors, which commonly lead to budget stress or buyer remorse:

- Ignoring variable-rate clauses that can escalate installments once central banks adjust policy rates.

- Underestimating insurance by assuming premiums match low-capacity scooters while purchasing a sport tourer.

- Accepting hidden add-ons such as credit-life policies you do not need or low-value extended warranties.

- Skipping the amortization schedule so you fail to identify months with larger balloon or annual charges.

- Missing payment reminders because you rely solely on paper statements rather than app notifications.

Mitigate each risk by configuring alerts within your chosen calculator and calendar.

When Free Calculators Are Not Enough

Free tools provide an excellent starting point, yet they lack advanced analytics like stress testing against interest-rate hikes, multi-currency support, and detailed tax treatment.

If your planned loan exceeds five years or includes currency exposure, common in cross-border purchases worldwide, consider professional software or consult a certified financial planner to validate the numbers.

Conclusion

Online simulation transforms motorcycle financing from guesswork into a controlled, data-driven decision. Collect accurate figures, compare multiple loan scenarios, and integrate insurance before committing.

Armed with a realistic repayment plan and the seven practical steps above, you ride away confident that monthly installments and long-term costs align with your income and lifestyle.

Enjoy the journey, secure in the knowledge that thorough preparation today safeguards your financial freedom tomorrow.